Briefing on the Trial of Disputes over Financial Leasing Contracts in Shanghai Court from 2014 to 2018

Finance leasing, as a financial model integrating financing and merchandise, trade and technical services, effectively promotes the interaction between market funds and industries, and has become an important part of modern service industry and financial industry in China. In recent years, China's financial leasing industry has been developing at a sustained and high speed. In August 2015, the General Office of the State Council issued Guiding Opinions on Promoting the Healthy Development of Finance Leasing Industry, which clearly pointed out that "Finance Leasing plays an important role in promoting industrial innovation and upgrading, broadening financing channels for small and medium-sized enterprises, promoting the development of emerging industries and promoting economic restructuring". As an important financial way to serve the real economy, its position in the social economy has been further enhanced. According to statistics, by the end of 2018, the number of financial leasing enterprises in China (excluding single project companies, branch companies, SPV companies and overseas acquisition companies) has reached more than 10,000, and the total amount of financial leasing business has reached about 6.65 trillion yuan. There are about 2210 financial leasing enterprises in Shanghai, ranking first in the country. At the same time, the number of financial lease disputes that have come into litigation has increased year by year, and it has become a major type of financial disputes that people's courts hear. The legal system supply of financial lease, self-discipline of enterprise market and supervision and management reflected in the trial of the case need to be solved urgently. The trial of disputes over financial leasing contracts in Shanghai Court from 2014 to 2018 will be reported as follows.

I. Characteristics of Disputes over Financial Lease Contracts

(1) Both the number of cases and the standard amount are increasing

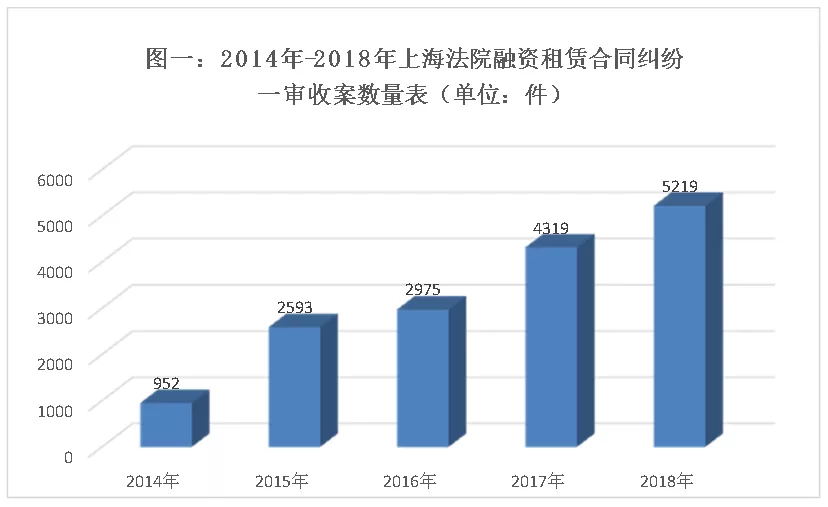

From 2014 to 2018, the courts of the whole city accepted 16,055 cases of financial lease contract disputes in the first instance, and concluded 15,667 cases, with the closing rate of 97.58% in the same period. The number of cases received increased year by year, including 952 in 2014, 2,593 in 2015, 2,975 in 2016, 4,319 in 2017 and 5,216 in 2018 (see figure 1).

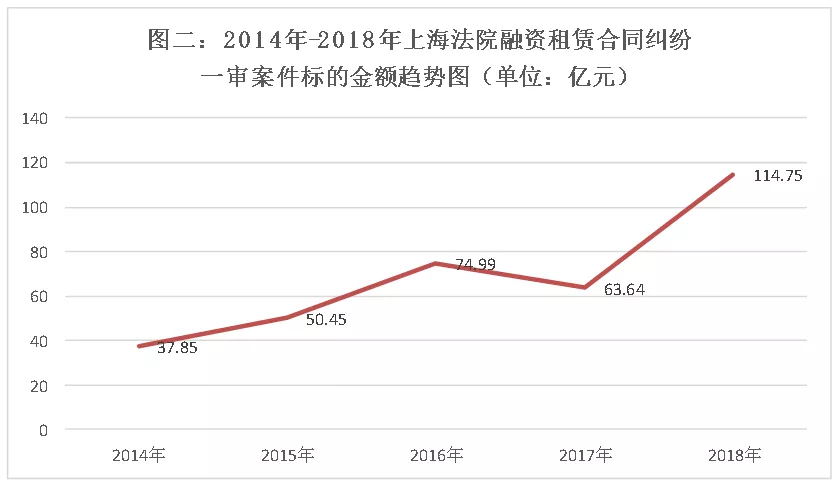

Judging from the amount of the object of the case, the total amount of the object of the case is 34.167 billion yuan (see figure 2). The number of cases and the total amount of the standard cases rank third in the first instance of financial and commercial cases accepted by the Shanghai Court.

(2) Concentration of types of litigation disputes

Rent arrears by lessees are the most common cause of disputes. As a plaintiff, the lessor, i.e. the financial leasing company, sues the lessee for rent, overdue interest, default fee and other rental costs, which accounts for the vast majority of cases. It can be seen that the main operational risk of financial lease is still the lessee's credit default. In the lawsuit, the defendants, such as the lessee, buyback and guarantor, have similar defense reasons against the lessor's right of rent claim and tend to be stereotyped. Among them, the reasons for the lessee's defense are mostly the objection to the quality of the leased goods, the objection to the residual value of the leased goods and the objection to the amount of the rent. The reasons for the buyback are mainly the objection to the validity of the buyback contract, the repeated claims of the lessor, the objection to the conditions of the buyback, the objection to the price of the buyback and the objection to the delivery of the leased goods. The main reason for the guarantor's defense is the objection to the validity of the guaranty contract.

(3) Relative concentration of cases

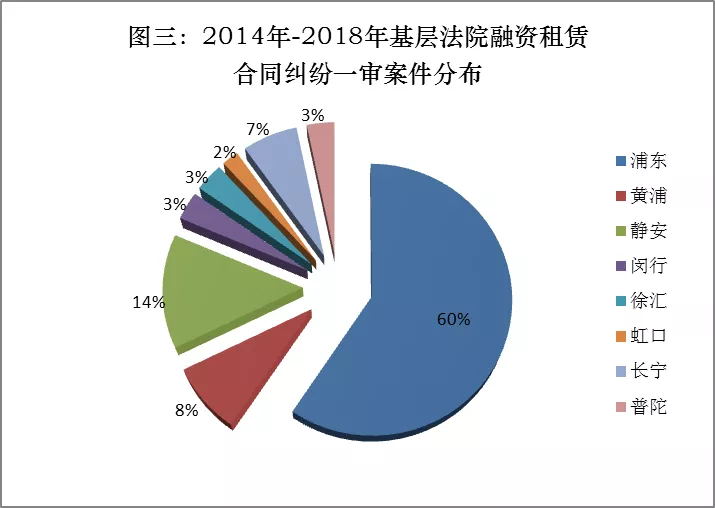

Based on the consideration of controlling operation risk and litigation cost, financial leasing company not only requests the lessee to provide as many guarantees as possible, but also agrees to be under the jurisdiction of the court of the lessor's location or the place where the contract is signed (often the lessor's location), which makes the disputes of financial leasing contract obvious. Characteristic of the location of the financial leasing company. As far as Shanghai courts are concerned, the financial leasing cases in Pudong New Area are the most, accounting for 60% of the total cases, followed by Jing'an District, Huangpu District and Changning District, accounting for 14%, 8% and 7% of the total cases respectively (see figure 3).

(4) The widespread existence of trial by default

Financial leasing cases may involve many parties such as lessees and guarantors, and financial leasing companies carry out business with cross-regional and decentralized characteristics, so the parties involved in the cases are generally scattered throughout the country. The lessee is mostly small and medium-sized enterprises with financing needs, while the guarantor is mostly the legal representative of the lessee or the employees of the enterprise, the related parties and other individuals, so the economic ability to resist risks is relatively weak. Once the lessee has difficulty in operation and the capital chain is broken, the lessee may transfer the lease to avoid debt, and the guarantor may transfer the secured property or escape. As a lessor, the financial leasing company can not grasp the situation of the lessee and the guarantor in time, and the legal service address is not stipulated in the financial leasing contract. As a result, after prosecution, the court often needs to mail some or all of the defendants several times, and the service of the announcement also happens from time to time, and even if the service is successful, some of the defendants also need to serve. The trial was held in absentia for various reasons. As far as the financial lease disputes cases tried by Shanghai Court in 2018 are concerned, the absence trial is widespread, objectively lengthening the time limit for handling cases and affecting the trial efficiency.

(5) It is more difficult to withdraw cases

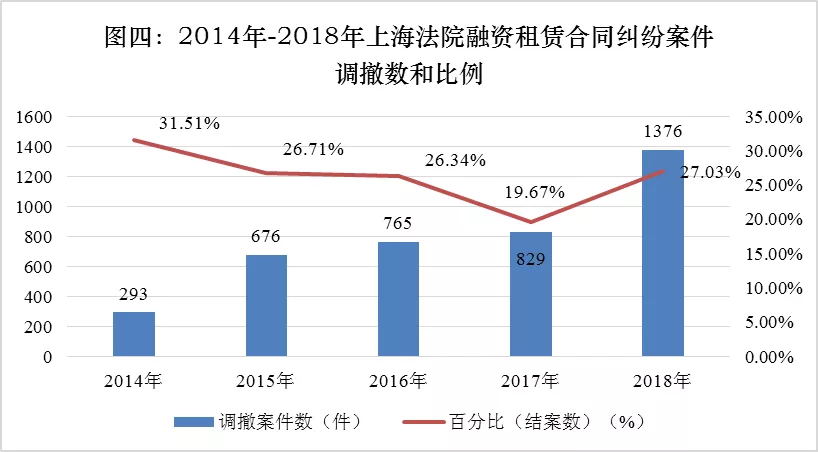

Because of service, deterioration of the lessee's business conditions, and even the escape of lessees and guarantors, it directly hinders the court's mediation of cases. Therefore, during the period of 2014-2018, Shanghai courts still use judgment as the main mode of such disputes, accounting for 74.74% of the total number of cases. Although the number of cases of mediation and withdrawal has increased year by year, the overall rate of mediation and withdrawal has shown a downward trend (see figure IV). Apart from the service of announcements and other reasons, this is mainly due to the deterioration of the lessee's business and serious liabilities, the lessor has no confidence in the lessee, it is difficult to accept the lenient repayment period mediation scheme proposed by the lessee, hoping to apply for implementation as soon as possible after the judgment according to law.

II. Research and Judgment of Dispute Cases in Financial Lease Contracts

(1) The number of financial leasing cases will continue to grow under the guidance of macroeconomic and financial policies

The object of traditional financial leasing is focused on the special equipment and other means of production in the real industry, such as excavators in the construction industry, high-precision printing equipment in the printing industry and so on. Influenced by the adjustment of domestic industrial structure and the slowdown of infrastructure demand, the fluctuation of related real industries has a great impact on the normal operation and solvency of lessees, which leads to a large number of financial lease disputes litigation. However, with the adjustment of industrial structure, the state has issued intensive policies to encourage the healthy development of financial leasing industry. Financial leasing will operate in many public areas, such as agricultural machinery, investment in science, culture, education, health and infrastructure, and will be distributed to high-end industries such as electronic information, big life, health, energy conservation, environmental protection and new energy. Bureau, business scope will accelerate expansion, industry docking will further accelerate. Affected by this, it is expected that the number of litigation cases of financial lease contract disputes will continue to increase in general, and disputes will gradually extend to emerging industries.

(2) The innovation of financial leasing transaction structure will lead to more complicated legal relationship involved in litigation.

The basic transaction structure of financial lease involves the tripartite subjects of lessor, lessee and seller, and involves two kinds of legal relations, namely, the legal relationship of financial lease between lessor and lessee, and the legal relationship of sale between lessor and seller. Based on the demand of financial innovation and market possession, the lessor designs a variety of more complex financing products, such as leveraged leasing, project leasing, risk leasing and so on, on the basis of the basic transaction structure of financial leasing. In order to maximize the protection of the lessor's rights and interests, lessors often adopt the way of increasing credit measures to bring repurchases and guarantors into the trading system of financial leasing. In practice, in order to meet its financing needs, the lessor may transfer the lease income right under the financial lease contract to the outside world. At this time, it may also involve the interests of the third-party private equity fund and the investors behind it. Therefore, the new type of financial leasing products involve more diverse subjects, resulting in more complex legal relations in financial leasing transactions.

(3) The trend of diversification of leasehold types will make the issue of publicity of ownership more prominent

Financial leasing is a transaction mode based on the separation of ownership and usufruct of leased property. The ownership of the lease belongs to the lessor, but its actual possession, use and income are all enjoyed by the lessee. Because the leased property is mostly movable property, and the transfer of ownership of movable property is based on delivery as a public requirement, the separation of ownership and use right of leased property makes it possible for the lessee to dispose of the leased property without authorization at any time. If the third party acquires the leased property in good faith, it will have a significant impact on the security of financial leasing transactions. In the current financial leasing transactions, the means for lessors to publicize the ownership of movable property leases are relatively limited, and the lease registration system is in the exploratory stage. At present, as the business field of financial leasing expands and extends to life, consumption and emerging areas, leased goods are showing a variety of characteristics, such as production equipment, consumer products, equipment, rights and even biological resources, which are difficult to transfer. Under such circumstances, how to establish a unified publicity mechanism of ownership registration and clarify the effectiveness of registration, and prevent the risk of financial leasing transactions, has become a difficult problem in hearing such cases, which needs to be solved urgently.

(4) Increasing financial functions may lead to an increase in financial leasing cases that are not in accordance with the actual situation

With the increasing function of financing instruments, the purpose of financial leasing business has changed from upgrading equipment to upgrading asset leverage ratio and maximizing asset activation in order to obtain financing. Financial leasing has become a tool for other real transaction purposes in the course of business development, and the legal relationship involved does not match the name. In the current trial practice, the most important manifestation is the case of financing lease, which is actually a loan case. The lessor and the lessee make use of the financing attributes of the financial leasing business to fabricate or falsify the leases, intentionally pursue or conceal the intentions of both parties to borrow and borrow funds, in order to avoid the industry supervision and legal risks. Specifically manifested in the signing of financial lease contracts with non-existent leases, or exaggerating the value of leases, forging lease invoices, or using equipment whose value is difficult to assess, transfer, possession, specificization or value is consumed with use, whose surface value is inconsistent with the actual value as leases. In addition, some cases are manifested in the name of financial lease, investment or sale. Because of the relevant provisions of judicial interpretation, the defendant will mostly defend with substantive legal relationship. Under the background of strengthening the purpose of financing in various industries, the number of cases of this type will increase.

III. Problems and Suggestions on Dispute Cases of Financial Lease Contract

(1) Problems and Suggestions on Traditional Financial Leasing Cases

1. The terms of the contract are ambiguous

First, the nature of down payment and margin is unclear. The financial lease contract stipulates that the lessee shall pay a certain amount of down payment and deposit to the lessor when signing the financial lease contract, but the nature and purpose of down payment and deposit are not clearly stipulated. Whether the down payment and the deposit are used as prepaid rent to offset the rent owed by the lessee, or as an additional cost to the lessor independently of the rent, there is often much controversy among the parties concerned.

Second, the way to determine the residual value of leased property is not clear. Leasing property is the guarantee of rental creditor's rights. If the lessor claims to cancel the contract, recover the leased property and compensate for the loss, it needs to determine the residual value of the leased property. However, in practice, there is no clear agreement on the evaluation method or estimation method of residual value of leased property in financial lease contracts. Once disputes arise, it is often necessary to entrust a third party to evaluate, which leads to prolonged litigation cycle and unnecessary depreciation loss of equipment.

Suggestions: The lessor should improve the contract terms, focusing on the provisions affecting the important rights and obligations of the parties, such as down payment, nature and use of the deposit, the relationship between the quality of the leased goods and the payment of rent, the exercise of the right to claim, the liability for breach of contract, and the way to evaluate the residual value of the leased goods.

2. Defects in contract performance

One is that the rent charged by the lessor is not standardized. Generally speaking, the down payment and rent of the financial lease shall be paid by the lessee to the lessor according to the contract. However, in some cases, there is a rent payment mode in which the lessee entrusts the supplier to transfer the rent. The lessor expressly agrees or impliedly approves the rent, while the supplier fails to pay the rent to the lessor in time or withholds the rent without authorization after collecting the rent, which causes the lessor to claim the rent to the lessee through litigation. In addition, in individual cases, there are also cases in which the supplier and the lessee enter into separate loan agreements after the down payment has been made by the supplier on behalf of the lessee.

Second, the lessee neglects the quality inspection of the leased property. Most of the lessees are small and medium-sized enterprises with capital needs. Their legal and contractual awareness is not strong. It is easy to neglect the quality inspection of the leased goods and accept the leased goods directly. In some cases, the lessee confuses the financial lease with the ordinary lease, or mistakes the three legal relationships of the seller, lessor and lessee of the financial lease as simple loan or sale relationship. After finding out the problem of the quality of the lease material, the lessee confronts with the refusal to pay the rent and sues the lessor for the right of rent claim. This is the main defense in the lawsuit.

Suggestions: Lessors should enhance service awareness, actively improve financial leasing services, provide safe and convenient rent payment methods for lessees, avoid unnecessary intermediate circulation link of rent payment, and prevent the occurrence of third-party interception rent to magnify financing risks. The lessee should enhance legal awareness, carefully check whether the model of the lease delivered is in conformity with the financial lease contract, and strengthen the quality inspection of the lease delivered.

3. Disposal of breach of contract is controversial

One is that the lessor withdraws the lease item by itself. As the dominant party in the contract, the lessor usually stipulates in the contract terms that when the lessee breaches the contract, the lessor can recover the leased property. In case of the fact that the lessee breaches the contract, the Lessor will directly take back the lease item without notifying the lessee. As for the lessor's unauthorized withdrawal of the leased property, the lessee considers that although it has indeed breached the contract, the lessor's unauthorized withdrawal of the leased property without warning and giving it a reasonable time limit is not in conformity with the relevant provisions of the law. The nature of the lessor's unauthorized withdrawal of the leased property is either a notification way for the lessor to urge the termination of the lease, or only a means for the lessor to exercise the right of defense in advance. The parties concerned have much controversy over it.

The second is that the lessor disposes of the leased goods by itself. After recovering the leased goods, some lessors sell and dispose of the leased goods at a discount on their own. Once involved in litigation, the lessee often objected to the disposal value of the leased property, believing that the value of the lessor's sale was significantly lower than its actual value. Because the lease has been monopolized and delivered to others, it is no longer possible to determine its actual value through third-party evaluation, which causes disputes and litigation risks.

Third, the agreed total rent and liquidated damages are obviously too high. Usually, the rent of a financial lease contract should be determined according to the most or all costs of purchasing the lease and the reasonable profit of the lessor, but the reasonable profit of the financial lease lacks the standard. For example, some financial lease contracts stipulate that the rent exceeds 24% or even 36% of the purchase price of the lease. When the lessee breaches the contract, it is also liable to pay the liquidated damages. For example, in the terms of the contract, the lessor not only stipulates the liquidation fee for the lessee's breach of contract, but also stipulates that the deposit paid by the lessee shall not be refunded when the lessee breaches the contract. This leads to the tenant's plea of excessive total rent and liquidated damages.

Suggestion: Firstly, the lessor, as the provider of standard contract, should prompt and explain the terms of the contract, especially the terms of exemption or limitation of its liability, at the request of the lessee, so as to avoid disputes over the validity of the terms of the contract. Secondly, the lessor should investigate the lessee's liability for breach of contract strictly in accordance with the contract and the law, so as to avoid the impact of illegal breach of contract on the normal production and operation of the lessee, resulting in further deterioration of the lessee's ability to perform the contract and intensification of contradictions and conflicts. Thirdly, the lessor should reasonably agree on rent and liquidated damages in the financial lease contract, reasonably determine the liquidated damages standard, and restrain the bad trend of high interest.

(2) Problems and Suggestions on Financial Leasing Cases of After-sale Rent-back

1. Lessor's negligence in examining the authenticity of leased property

After-sale leaseback takes the ownership of the lessee as the subject matter of financial lease. Whether the leased property really exists or not needs to be examined and confirmed by both parties in the process of contracting. Therefore, the tendency of refinancing and lightening the financial items is more likely to occur in the process of after-sale leaseback. For example, the leasehold does not exist in some after-sale leaseback contracts. When the lessee breaches the contract, the lessor brings a claim for rent. The lessee protests or counterclaims that the lease does not exist and requests confirmation of the invalidity of the after-sale leaseback contract. For example, the leasehold items stipulated in part of the after-sale leaseback contract are not clear. Usually, the lease subject matter stipulated in the lessee's own equipment or assets is only part of the equipment or assets. The lessor has not examined and determined the leased items, which causes the defect of the original ownership of the leased items by the third party. For reasons such as bona fide acquisition, disputes arise with the lessor. Financing lease has dual attributes of financing and financing. Therefore, if the lease does not exist or is not clear, it should be considered as financing without financing, which is essentially equivalent to borrowing and financing, deviating from the original intention of the design of financial lease system, and will shake its legitimacy foundation. In addition, whether the subject matter of the lessee's own limited disposition right can be transferred to the lessor as a lease is also controversial.

Suggestion: Although the law does not clearly stipulate the lessor's obligation to audit the leased property, the existence and specificity of the leased property is an important basis for identifying the legal relationship of after-sale leaseback. Therefore, the lessor should strictly examine the right vouchers (including purchase invoices, contracts, specifications, certificates, etc.) of the lessee (i.e. the seller) with the right to dispose of the leased property, check the authenticity of the leased property on the spot, and make a detailed inventory and identification of the leased property transferred and register it.

2. It is difficult to determine the actual value of the leased property

Under the direct-rent mode, leases are generally purchased from third-party sellers. If there is a dispute over the actual value of leases, it can be determined according to the market value of the leases and related purchase documents such as invoices. In the case of after-sale rent-back, because the seller and the lessee are the same subject, some leases are made by the lessee himself, and some leases are purchased from the second-hand market, the market value is difficult to judge, and there is no relevant purchase certificate to support, it is very easy to dispute. The determination of the real value of the leased goods involves whether the transfer price of both parties is reasonable. The relevant regulations of MOFCOM and CBRC require that the financial leasing company should have reasonable pricing basis for the purchase of the subject matter and not violate accounting standards as a reference. In such cases, the lessee tends to deny the legal relationship between the two parties on the basis of the mismatch or serious deviation between the actual value of the lease and the transfer price. The mismatch between the transfer price and the actual value of the leased property is manifested in two forms, namely "low-value high-buy" or "high-value low-buy". In the current cases of after-sale rent-back, because the lessor is in a dominant and powerful position, it mostly manifests as "half-price purchase", "differential purchase" and other "high-value and low-purchase" rent-back situations. Whether the nature of this act can be identified as "after-sale rent-back" depends on respecting the voluntary trading arrangements of commercial subjects without damaging the legitimate rights and interests of third parties, or whether it can be recognized as "after-sale rent-back". There are disputes about judicial intervention in order to violate the principle of fairness and the real intention of both sides is only to finance. In individual cases, there are also cases of low-value and high-buy. The lessee mostly defends the fact that the lessor borrows and lends in the name of after-sale leaseback and goes beyond the scope of business.

Suggestion: After-sale leaseback lessor should reasonably price the transfer price of the lease according to the extent to which it can guarantee the realization of its financing creditor's rights and the extent to which it can cover the creditor's rights. If necessary, qualified audit and evaluation institutions should be introduced to avoid the transfer price and actual value of the leased goods. Serious deviation caused controversy.

3. The ownership of the leased property has not been transferred to the lessor's name

In the after-sale leaseback transaction, the lessor's acquisition of ownership is an important legal feature to identify the financial lease transaction. Since the lease is always occupied and used by the lessee, it is necessary to combine the theory of delivery of real right with the fact of performance of the contract to determine whether the ownership of the lease has been transferred from the lessee to the lessor. For example, in the case of after-sale and leaseback of real estate as leasehold, registration is the effective requirement for the transfer of ownership of real estate in the Property Law of the People's Republic of China. Therefore, if the real estate cannot be transferred and the lessor knows it well when signing the contract, it should be determined that the true meaning of both parties is not financial lease, but rather financial lease. Capital lending. In addition, in some cases of after-sale leaseback, the leased property transferred by the lessee to the lessor is not the owner of the right to dispose of. Before the transfer, the leased property has the burden of right such as mortgage or the right to seize or detain. The lessee argues that it is not entitled to dispose. For example, if the lessor does not meet the statutory requirements for bona fide acquisition of the ownership of the leased property, It should also be recognized that it does not constitute after-sale rent-back.

Suggestion: In the after-sale leaseback business, besides reaching the agreement with the lessee to transfer the leased property, the financial leasing company should also attach importance to transferring the ownership of the leased property to the lessor's name by means of delivery of movable property and registration of real property, so as to reduce the risk of financial leasing transaction and ensure the safety of financial leasing transaction.

(3) Problems and Suggestions on the Case of Repurchase Financing Lease

1. The lessor is lazy to notify the buyer to fulfill the buyback obligation

In repurchase financial lease, the manufacturer or seller of leased goods not only assumes the role of seller, but also has the obligation to repurchase leased goods when the lessee defaults such as unpaid rent. The lessor and the buyback agree in the contract that the buyback obligation shall be fulfilled when the conditions for the buyback are fulfilled (if the rent overdue by the lessee reaches a certain time limit), after the lessor gives the buyback notice to the buyer. However, in practice, the lessor does not notify the buyer to fulfill the buyback obligation when the conditions for the buyback have been fulfilled. Instead, the lessor sends the buyback notice to the buyer after the expiration of the performance period stipulated in the financial lease contract. Because the contract stipulated repurchase price is linked to the time of the achievement of repurchase conditions, that is, the later the lessor sends the repurchase notice, the higher the repurchase price. Therefore, the buyback objected to the repurchase price in the trial, believing that the lessor neglected to notify it to fulfill its repurchase obligations and subjectively had the intention of raising the repurchase price. The lessor considers that notifying the buyback to fulfill the buyback obligation is the right entrusted to it by the contract. As long as the condition that the rent overdue by the lessee reaches the agreed days of the contract is satisfied, the lessor can choose to claim the rights and interests of the buyback at any time and cause disputes.

Suggestion: All parties to the contract should abide by the principle of good faith and perform the contract properly according to law. The lessor strictly abides by the contract stipulation, notifies the buyer to fulfill the buyback obligation in time when the buyback condition achieves, avoids the loss of the value of the leased property and the expansion of the buyback responsibility of the buyer. The buyback party should actively fulfill the obligations and responsibilities stipulated in the contract. When finding the achievement of the buyback conditions, it can actively negotiate with the lessor about the buyback matters and make timely derogation.

2. Non-delivery of leases in repurchase performance

If the lessee breaches the contract, the lessor sues the buyer for fulfilling the buyback obligation according to the agreement of the buyback contract. The repurchase contract stipulates that the lessor notifies the lessee to deliver the lease to the buyer, which belongs to the instruction delivery. If the lease has no possibility of delivery, whether the buyer still has to fulfill the buyback obligation. For example, during the trial, it was found that the lease item had been sealed up by the court or that there was a security right in the lease item, so the lessee could not actually deliver the lease item to the buyer. For example, in some cases, if the leasehold property is lost, can the buyback counteract the lessor's right of claim for repurchase? The controversy on this issue mainly involves the understanding of the nature of repurchase contracts. The lessor maintains that, based on the guarantee nature of the repurchase contract, the buyer's obligation to pay the repurchase money is to assume the guarantee liability, which has nothing to do with whether the lessee delivers the goods according to the instructions or whether the leased goods can be delivered, so the buyer should assume the responsibility of repurchase. The buyer argues that the essence of repurchase is a conditional contract of sale, and the subject matter should be considered as payment. Because the lease item can not be delivered, the buyer does not need to fulfill the obligation of repurchase.

Suggestion: The repurchase contract has the dual attributes of guarantee and sale contract. In the case of disputes over the application of the law, the lessor should improve the terms of the repurchase contract, clarify its effectiveness to the lessee, exercise the right of repurchase claim in time when the conditions for repurchase are successful, and keep the relevant evidence. In the process of signing the repurchase contract, the buyer should pay attention to the provisions concerning the feasibility control of the subject matter's recovery, and make a clear agreement on the risk liability of the loss and damage of the subject matter's repurchase.

(4) Problems and Suggestions on Financial Leasing of Special Leases

1. Can Consumables Be the Subject of Financial Lease

As a kind of lease legal relationship, the subject matter of financial lease legal relationship should have the characteristics suitable for lease. When the term of financial lease contract expires, it has the possibility of restoring the object. If, according to the characteristics of the subject matter, it can not be returned at the expiration of the term under normal use, it can not be objectively regarded as the subject matter of the financial lease relationship, and the corresponding legal relationship can not be recognized as the financial lease relationship. During the trial, it was found that some financial lease contracts stipulated that the lease items were "a batch of decorating materials" and some agreed that the lease items were "cement fenders". Because the lease items were consumables and unclear or unspecified, the lessor demanded the return of the lease items when the lessee breached the contract. The court finally decided that the disputed contract named financial lease was actually a loan. Payment contract. In addition, in order to circumvent the restrictive provisions on the subject matter of financial lease, some financial leasing companies set up trading companies separately, and engaged in installment payment sales contracts named retention of title for the subject matter involving paper, raw pulp and other consumables by means of trade. The defendant pleaded that the transaction was actually a loan.

Suggestion: Although broadening the financing channels of small and medium-sized enterprises is one of the objectives of current financial reform and innovation, and serving the real economy "from emptiness to reality", while innovating and reforming the system, lessors should pay full attention to the characteristics of financial lease subject matter suitable for leasing and operate legally and in accordance with the regulations in the process of expanding their business.

2. Exercise of Mortgage Right of Motor Vehicle Financing Lease

In the case of motor vehicle financing lease, it is found that the lessor and the lessee sign a financial lease contract, which stipulates that the lessor purchase motor vehicles from the seller and lease them to the lessee for use in accordance with the requirements of the lessee. Considering the convenience of vehicle use, after the lessor pays the vehicle transfer price to the seller, the motor vehicle is registered directly under the lessee's name, but the actual owner is the lessor. At the same time, the lessor and the lessee sign a mortgage agreement, and the lessee mortgages the motor vehicle to the lessor as a mortgagor and registers the mortgage. After the lessee breaches the contract, the lessor appeals to the court to request the lessee to pay all the unpaid rent stipulated in the contract, and at the same time requests the exercise of mortgage on motor vehicles. Whether the mortgage can be exercised under such circumstances is controversial.

One view is that Article 9, paragraph 2, of the Supreme People's Court's Interpretation of Several Questions Concerning Disputes over Financial Lease Contracts, recognizes the way in which the lessor registers the leased property under the name of the lessee, and there is no legal obstacle to the mortgage of the leased property. The lessor has the mortgage right registered publicly, and his claim for the mortgage right has the legal basis. Another point of view is that the purpose of signing mortgage agreement and registering mortgage between lessor and lessee is to publicize the lease and prevent the lessee from disposing of the lease without authorization. Both parties have no desire to establish mortgage guarantee, which is a false declaration of intention. And exercising the mortgage means rescinding the contract. According to the relevant judicial interpretation, we can not advocate paying all unpaid rent in advance and exercising the mortgage at the same time.

Suggestion: Based on the professional characteristics of financial lease disputes, lessors should design reasonable litigation claim scheme according to law in order to protect their legitimate creditor's rights and reduce unnecessary litigation risks.

IV. RELATED SUGGESTIONS

(1) Improving the laws and regulations on financial leasing

Chapter 14 of the Contract Law of the People's Republic of China and the Interpretation of the Supreme People's Court on Several Questions Concerning the Trial of Disputes over Financial Lease Contracts are the main bases for the court to hear financial lease disputes at present. With the intensive introduction of relevant measures to speed up the development of financial leasing and financial leasing industry, the explosive high-speed growth trend of financial leasing industry has been slowed down due to the stricter supervision and the requirement of returning to the origin of leasing and serving the real economy, but the business scale of financial leasing industry continues to grow, and the new type of financial leasing transaction continues to grow. The mode is also constantly emerging, and the courts are facing many procedural and substantive difficulties in hearing cases of financial lease contract disputes. In view of the important position of financial leasing industry in China's market economy, we should improve the relevant supporting legal system as soon as possible in view of the current development of financial leasing in China, especially in view of the legal relationship of new types of financial leasing, promulgate legal and judicial interpretations as soon as possible, protect the rights and interests of all parties fairly, and give full play to the legal role in the financial leasing market. The standardization, guarantee and guidance function of the financial leasing business can optimize the industrial structure and provide strong support for the innovative development of the financial leasing business.

(2) Strengthening the construction of risk control system

Financial leasing companies should standardize business processes and establish a sound internal risk control system. Specific manifestations are as follows: before the signing of the contract, the materials reflecting the lessee's operating conditions, business licenses of commercial credit, tax registration certificates, bank credit repayment records, financial statements, capital verification reports and so on should be carefully examined, and the credit rating mechanism of the lessee should be established; at the time of the signing of the contract, the quality of the lease material and the payment of rent should be closely examined. Provisions such as the form of claim right, liability for breach of contract and the determination of residual value of leased property should be stipulated to clarify the rights and obligations of all parties; actively coordinate participation in inspection or on-site supervision of the delivery of leased goods in the course of performance; establish a normal communication mechanism with the lessee, and grasp the business status of the lessee in real time with the help of effective resources. And the use of leased goods. The lessee should enhance the awareness of law and risk prevention, pay attention to the protection of his rights under the contract on the basis of careful financing decision-making, and ask the financial leasing company to explain the relevant provisions when necessary. Buyers and guarantors should strengthen risk pre-judgment, and in the process of fulfilling financial lease contracts, they should strengthen the grasp of information about the lessee's operating conditions, performance and the status quo of leased goods.

(3) Establishing and perfecting a complete trading mechanism

Most of the leases are movable property. Compared with the real estate registration agencies, there are many and scattered movable property registration agencies, which have a relatively high possibility of triggering transaction risks. In view of the lack of a unified publicity system for property ownership registration, it is suggested to improve the publicity system for financial lease of the People's Bank of China Credit Inquiry Center, guarantee the rights of financial leasing companies to leases, effectively reduce the registration and inquiry costs of the parties, and enable third parties to know the actual rights of leases through the above-mentioned system. Conditions, reduce the risk of transactions involving leased goods, and ensure the safety of transactions. In view of the lack of channels for financial leasing companies to deal with leases, it is proposed to establish a fair and efficient residual value assessment mechanism for leases, and to foster a secondary leasing market, so as to effectively resolve the disputes between financial leasing companies and lessees over the residual value of leases and realize the reuse of leases after recovery.

(4) Strengthen industry self-discipline and supervision

Financial leasing industry associations play an important role in promoting information exchange among enterprises, standardizing and coordinating industry development. As far as the experience of developed countries in financial leasing industry is concerned, financial leasing industry associations play a bridge and link role between the industry and domestic and foreign governments and organizations. Based on the industry association's familiarity and understanding of industry development, it has the most intuitive understanding of industry issues, can effectively reflect the general needs of enterprises to government departments, and coordinate among the industry participants under the authorization of the government, and strengthen the industry's internal self-discipline and self-incentive. It is suggested that financial leasing industry associations play an important role in promoting enterprise communication, strengthening intra-industry communication, reflecting industry requirements, unifying industry rules, standardizing industry operation and preventing industry risks. On the basis of industry self-discipline, the regulatory authorities should further strengthen the norms and guidance of financial leasing companies in developing new types of financial leasing business, maintain the order of financial leasing market, and effectively guard against financial risks while serving to safeguard the economic development of entities.